![]()

Will Inflation Be Permanently Temporary?

Submitted by JMB Financial Managers on November 2nd, 2021

Authored by: Kezia Samuel, Guest Author

Key Takeaways

- Inflation remains an ongoing concern in 2021.

- While inflation is higher and likely to remain elevated due to challenges created by the pandemic, a look into the structural composition and the types of inflation may provide insight into how high inflation may go.

Inflation remains a topic of concern in 2021 as the prices of goods and services have continued to increase. The September inflation report showed consumer prices rose at 5.4%.1

With elevated inflation, it’s not surprising for investors to wonder how long this trend is going to last. The Federal Reserve has acknowledged that inflation expectations have risen, but have qualified the recent inflation spike as “transitory,” or in other words, temporary. A deeper look at how inflation is measured may provide some insights into why the Fed takes this stance.

The inflation rate measures price changes for a basket of goods and services that typically behave in different ways. Inflation rates for some categories of goods and services are relatively flexible or responsive to economic conditions, implying they are “cyclically sensitive.” These include categories such as food, travel, energy and cars. This segment of inflation can see large swings in prices and contributes 38.0% of inflation measurement.2 In the latest reading, prices of energy and used cars both increased nearly 25.0% year-over-year as of September.3

On the other hand, the inflation rate for other categories, such as medical and financial services, tend not to vary with the state of the economy and are relatively “acyclical.” This stable segment of inflation makes up 62.0% of inflation prices. In contrast to rising energy and car prices in September, medical services saw an increase of 0.9% year-over-year.

The key point being much of the spike in inflation has come from the smaller cyclical segments, which often is short-term in nature than longer lasting from the larger acyclical segment. In short, the structural composition of how inflation is measured may limit how high inflation can go.

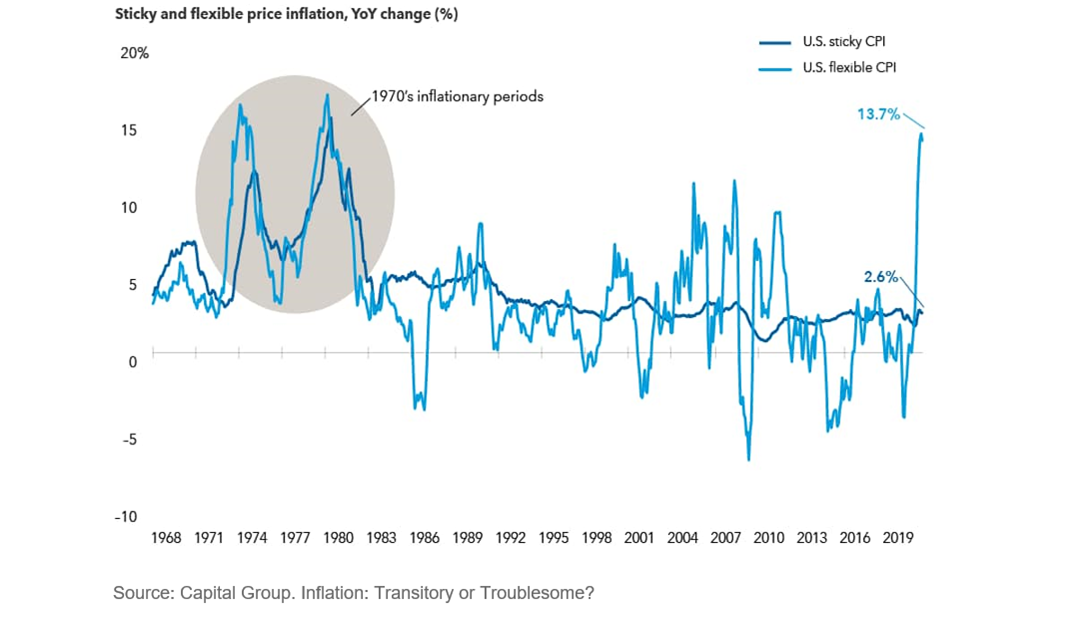

Another way to see this is based on the chart on the next page by Capital Group with data from the Federal Reserve of Atlanta.4 They looked at two kinds of inflation: sticky and flexible.

If price changes for a particular inflation component occur less than every 4.3 months, that component is a “sticky-price” good. Sticky categories include medical expenses and financial services. On the other hand, goods that change prices more frequently are considered “flexible-price” goods. Flexible goods include food, energy and cars, where prices can experience wild swings and are much more closely tied to the state of the economy—as

consumers recently have witnessed. As of August 2021, flexible inflation has climbed to nearly 14.0% and bears close resemblance to inflation rates of 1970. However, sticky inflation remains subdued and gained 2.6% year-over-year, a stark contrast to the scary inflationary periods of 70s.

The drivers of flexible inflation are deeply rooted in supply chain disruptions due to the pandemic. A simple example would be new and used vehicles. During the pandemic people no longer felt comfortable taking public transportation and started looking for new and used cars. Demand for vehicles spiked and caught both chip and car makers off guard as many factories were entirely shutdown. As a result, used car prices rose sharply. History has proven such supply and demand disruptions are efficient at correcting over time. This can be seen in the price decline for used cars, which has fallen sharply from a 42.0% year-over-year increase as of July to 25.0% in September.5 While autos are the most glaring example, there are many more examples of this type of flexible inflation—like lumber and other commodities used in home building—all of which have fallen from peaks since earlier this summer.

In conclusion, while the definition of “transitory” appears to be longer than many were hoping it would be, flexible inflation or cyclical categories have clearly experienced sharp price increases due to transitory reasons like pandemic-related shortages. Nevertheless, inflation is expected to be higher than pre-pandemic levels and further choppiness remains possible, as the global economy continues to deal with fallout from the pandemic, which is unlikely to resolve soon. For those concerned about elevated inflation, take some consolation in the fact inflation has stayed below 5.0% the vast majority of the time during the last 100 years.6

To add further context, elevated inflation appears alarming given it is rising from very low levels of below 2.0% in the aftermath of the global financial crisis.The key going forward will be to watch if sticky inflation also moves higher.

In short, as Richie Tuazon at Capital Group shares, “flexible inflation is transitory, but sticky inflation could be troublesome.”

--

About the Author

Kezia Samuel is Vice President of Client Portfolio Management at AssetMark. She is responsible for monthly and quarterly commentary on market performance and current events for advisors and their clients.

[1] https://www.bls.gov/news.release/pdf/cpi.pdf

[2] Goldman Sachs Asset Management SAS Market Strategy. Setting the Stage: Market Know-How

[3] https://www.bls.gov/news.release/pdf/cpi.pdf

[4] https://www.capitalgroup.com/advisor/insights/articles/inflation-transit...

[5] https://www.businessinsider.com/used-car-price-increase-slowing-down-buy...

[6] https://www.capitalgroup.com/advisor/insights/articles/inflation-transit...

IMPORTANT INFORMATION

This is for informational purposes only, is not a solicitation, and should not be considered investment, legal or tax advice. The information in this report has been drawn from sources believed to be reliable, but its accuracy is not guaranteed, and is subject to change. Investors seeking more information should contact their financial advisor. Financial advisors may seek more information by contacting AssetMark at 800-664-5345.

Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss. Actual client results will vary based on investment selection, timing, market conditions, and tax situation. It is not possible to invest directly in an index.

Investments in equities, bonds, options, and other securities, whether held individually or through mutual funds and exchange traded funds, can decline significantly in response to adverse market conditions, company-specific events, changes in exchange rates, and domestic, international, economic, and political developments.

AssetMark, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. AssetMark and third-party service providers are separate and unaffiliated companies. Each party is responsible for their own content and services.

©2021 AssetMark, Inc. All rights reserved.

JMB Financial Managers Mid-Year Review for 2025

Click the button below to download a pdf of insights and predictions for the rest of the year.