![]()

How Life Expectancy is Changing the Need for Retirement Planning

Submitted by JMB Financial Managers on August 13th, 2020

For much of our history, retirement in America was defined in terms of its relationship to full-time participation in the work force. An individual would work until a certain age and then leave employment to spend time on personal endeavors. Declining health often made retirement short, so retirement planning was about saving enough to guarantee minimal survival for a relatively brief period.

Today, society is beginning to recognize that the traditional view of retirement is no longer applicable. Some individuals, for example, are voluntarily choosing to retire early in their 40s or 50s. Others, because they enjoy working, choose to remain employed well past the traditional retirement age of 65. Retirement is now often defined by activities such as travel, returning to school, volunteer work, or the pursuit of favorite hobbies or sports.

This new concept of retirement, with all its possibilities, does not happen automatically. Many of the issues associated with retirement, such as ill health and the need for steady income, still exist alongside the lighter more enjoyable aspects of those years. With proper planning, however, all your needs can be met.

Addressing Longer Life Expectancy in Your Retirement Plan

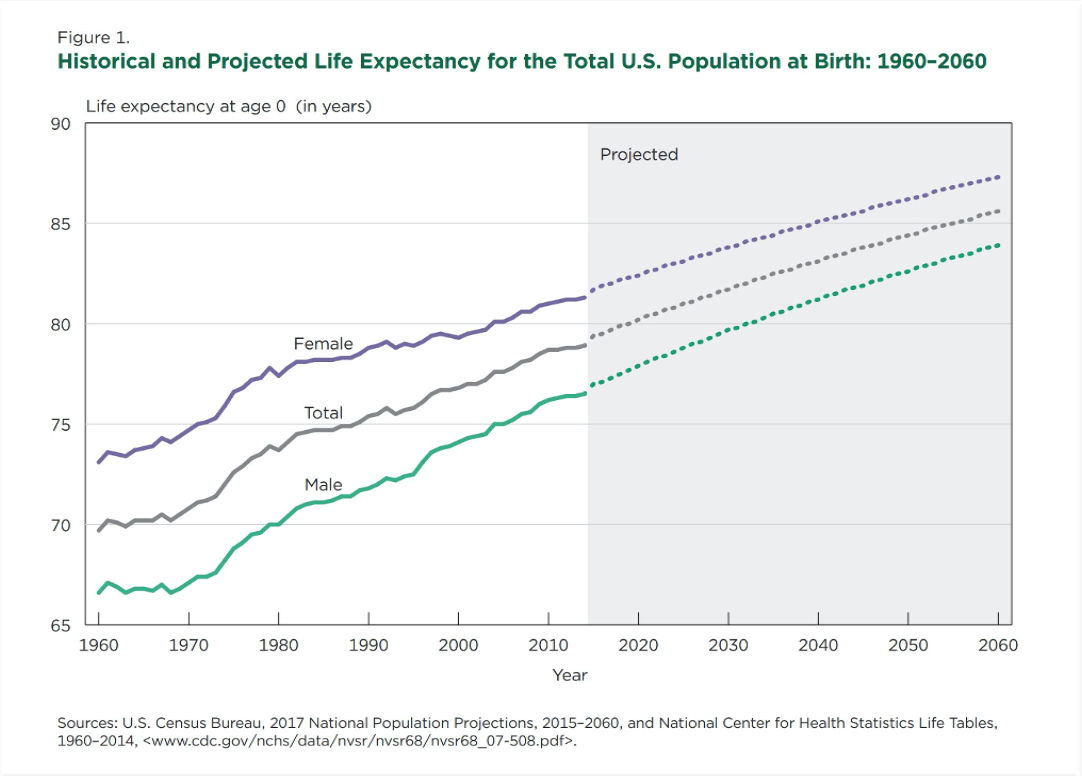

The single most important factor in this changed retirement picture is the fact that we now live much longer than before. A child born in 1960, for example had an average life expectancy of 69.7 years. For a child born in 2015, however, average life expectancy had increased to 79.4 years.1 The following graph illustrates this change and the projected increase in life expectancy through 2060.

Planning for a much longer life span involves addressing problems not faced by earlier generations. Learn more about some of the key areas to focus on when developing your retirement plan.

3 Areas to Focus on When Developing Your Retirement Plan

Paying for Retirement

Obtaining a steady income is often the number one priority in retirement planning. Longer life spans increase the issue of inflation on fixed dollar payments, as well as the possibility of outliving accumulated personal savings. Social Security retirement benefits and income from employer-sponsored retirement plans typically provide only a portion of the total income required for individuals to live a comfortable retirement. If income is insufficient, a retiree may be forced to either continue working or face a reduced standard of living. Preparing in advance for what your source of income will be during retirement and how much you will need will help you avoid any surprises or shortages.

Paying for Healthcare

The health benefits provided through the federal government’s Medicare program are generally considered to be only a foundation. Often a supplemental Medigap policy is needed, as is a long-term care policy, to provide necessary benefits not available through Medicare. Health care planning should also involve considering a healthcare proxy (allowing someone else to make medical decisions when an individual is temporarily incapacitated) as well as a living will that expresses an individual’s wishes when no hope of recovery is possible. If you have questions regarding the healthcare options during retirement or need assistance syncing your retirement, healthcare, and legal planning teams reach out to our team today to discuss your situation.

Paying for Housing

Paying for housing during retirement is a multifaceted decision and involves not only the size and type of home (condo, house, shared housing, assisted living) but also its location. Other factors such as climate, proximity to close family members and medical care are often important to consider. Looking to spend your retirement somewhere new? Check out the Top 10 Best Places to Retire in 2020.

If you’re planning on staying put there are other choices to be made. Completely paying off your home loan can reduce monthly income needs which is important during those golden years. No matter where you decide to live during your retirement years, having a plan to pay for it should be a fundamental part of your retirement plan.

Develop a Retirement Plan to Match Your Goals

Developing a successful retirement plan involves carefully considering a wide range of issues and potential problems. Finding solutions to these questions often requires both personal education and the guidance of knowledgeable individuals from many professional disciplines, including a Certified Financial Planner. The key is to begin planning as early as possible. If you’re ready to get started or wish to discuss your specific situation, reach out to us and a retirement expert from our team will be in touch shortly.

Citations:

--

About the Author

Jack Brkich III, is the president and founder of JMB Financial Managers. A Certified Financial Planner, Jack is a trusted advisor and resource for business owners, individuals, and families. His advice about wealth creation and preservation techniques have appeared in publications including The Los Angeles Times, NASDAQ, Investopedia, and The Wall Street Journal. To learn more visit https://www.jmbfinmgrs.com/.

Jack Brkich III, is the president and founder of JMB Financial Managers. A Certified Financial Planner, Jack is a trusted advisor and resource for business owners, individuals, and families. His advice about wealth creation and preservation techniques have appeared in publications including The Los Angeles Times, NASDAQ, Investopedia, and The Wall Street Journal. To learn more visit https://www.jmbfinmgrs.com/.

Connect with Jack on LinkedIn or follow him on Twitter.

JMB Financial Managers Mid-Year Review for 2025

Click the button below to download a pdf of insights and predictions for the rest of the year.