![]()

The Hidden Risks of Passive Investing

Submitted by JMB Financial Managers on June 17th, 2025

It is no secret that investment dollars have been shifting from actively managed investments to passively managed investments (i.e., Index Funds). There’s one number that explains a good portion of this phenomenon: 13.80%. The compounded annual growth rate (CAGR) of the S&P 500 Index over the last 15 years ending December 31, 2024, was 13.80% per year. This high rate of return has given birth to, among other things, an explosion of exchange-traded market index funds seeking better performance.

The Rise of Passive Investing and Potential Risks

It is also no secret that investors have gone beyond merely shifting a portion of their portfolios to a bevy of low cost index funds - they have moved millions upon millions of dollars into passive mutual funds and asset allocation models.

I believe many of these investors have made their decisions to move into passive investments based on cost savings and achieving index returns, without fully understanding the long-term implications of their choices. This has the potential for long-term disappointment as a result. For example, a 2018 research study prepared by the Natixis Center for Investor Insight revealed that 64% of those polled believe that their index funds are less risky than active funds, and 71% think that index funds will help them minimize losses in down markets.

What You Need to Know About Passive Investing

In reality, passive funds have no built-in risk management, and they have become more and more risky over time, which is the exact opposite of what passive investors believe. An example of this would be the growth of technology stocks within the S&P 500 Index. At 29.3%, Technology is at its highest proportion of the S&P 500 since 2000, when the Internet Bubble popped and the market began a three-year losing streak. (The technology sector has the most volatility of any sector within the Index.)

Most investors have no idea that almost thirty percent of their investment in the Index is in one industry, and have no idea just how badly bear markets are apt to hurt their net worth, as in the Great Financial Crisis or the dot.com bubble of the late 1990s.

Passive Investing has become Passive Allocation

The more worrisome trend, in my view, is the shift to static asset allocation and other passive strategies, rather than the shift to index funds, per se. This can have a more powerful, negative effect on long-term investment results.

For example, in a landmark paper published in 1986, “Determinants of Portfolio Performance”, Gary P. Brinson, L. Randolph Hood, and Gilbert L. Beebower concluded that asset allocation is the primary determinant of a portfolio’s return, and in fact, it was 90% of the reason for a portfolio’s return. The “Brinson Study", as it is referred to, was revisited by Gary Brinson in 1991 and yielded similar results.

A more simplified conclusion from the study is that 90% of the return in an investor’s portfolio will be determined by the mix of stocks, bonds, commodities, currencies, and cash, while only 10% will be determined by which individual stocks or investment funds are chosen within each category, or the costs associated with purchasing them.

In 1997, William Jahnke published a critique of The Brinson Study and concluded, "Static asset allocation solutions are inferior to analytically linking, forward-looking, active asset allocation solutions. As an investor’s circumstances, the economic environment, and market conditions change, so also should the investor’s asset allocation.”

Another widely cited study of pension plan managers said that 91.5% of the difference between one portfolio’s performance and another’s performance is explained by their asset allocation.

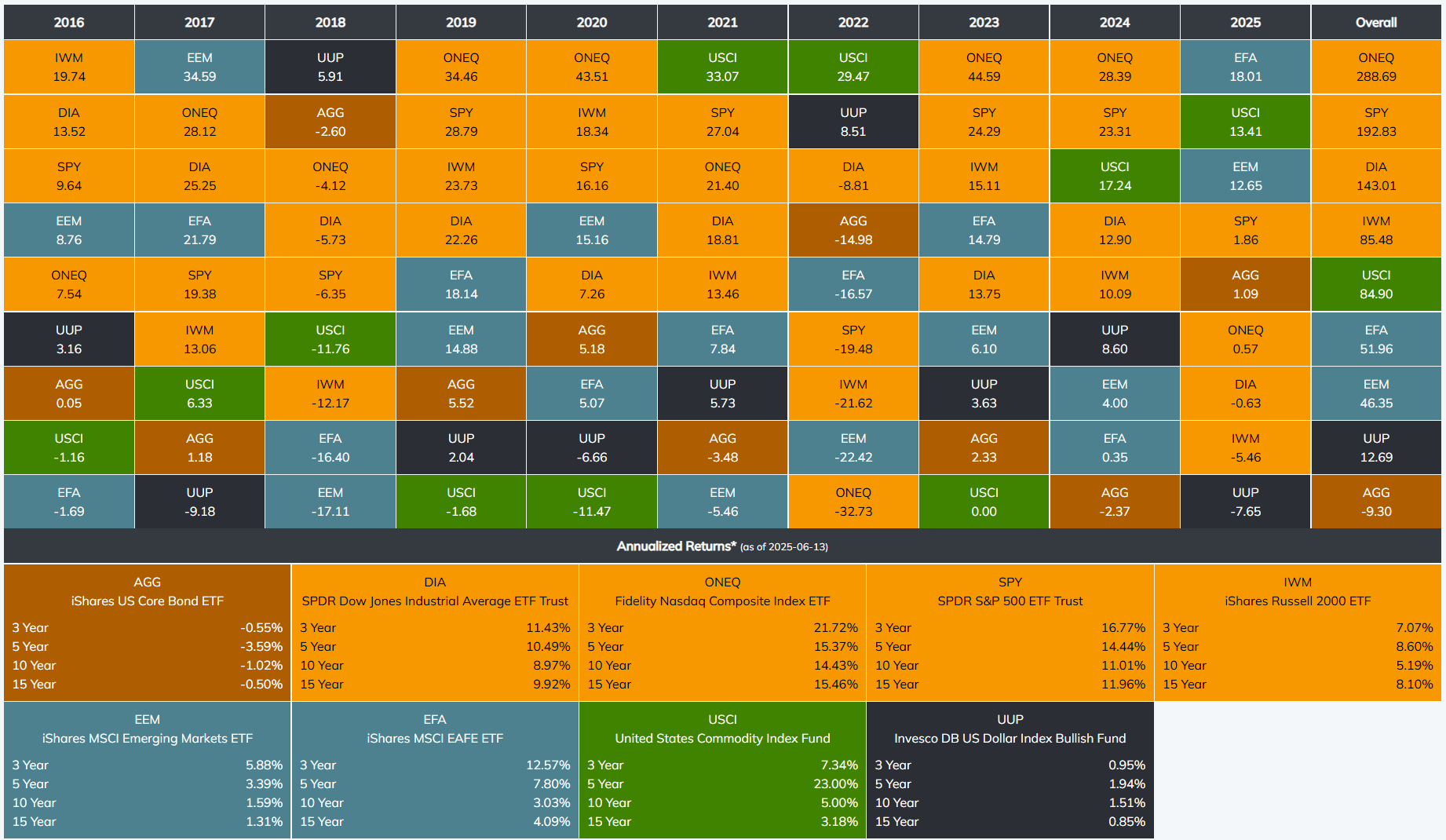

In other words, returns are based on "being in the right place at the right time" over the long run. The returns by asset class in the past 10 years can be seen in the chart below.

(Source: Nasdaq.dorseywright.com. AGG represents the Barclay’s Aggregate Bond Index; DIA represents the Dow Jones Industrial Index; EEM represents the MSCI Emerging Markets Index; EFA represents the MSCI Developed Markets Index; IWM represents the Russell 2000 Index; ONEQ represents the NASDAQ Composite Index; SPY represents the S&P 500 Index; USCI represents the US Commodity Index; UUP represents the US Dollar Index. Investors cannot invest directly in any particular Index. The returns shown represent past performance of an exchange traded fund, and past performance does not guarantee future results. The information presented is not a recommendation to buy or sell securities..)

As you can see, it was far more important to have avoided Bonds (AGG) and to have owned US Stocks (ONEQ, SPY, DIA, IWM) and Commodities (USCI) than it was to have chosen a particular stock or fund.

Yet, investors with a passive asset allocation strategy not only held a fixed amount of bonds for the entire decade, but they also sold their stocks and commodities to purchase more bonds when they rebalanced their accounts. This reduced their gains and increased their losses. Passive asset allocation dragged the 10-year investment portfolio returns down by its very nature.

Passive Investing is a Non-Strategy

Being passive as an allocation strategy is bothersome. It looks more like an "I-give-up strategy" than a means for optimizing returns. Oddly enough, it was Mao Tse-tung (who was hardly a capitalist) who famously stated, “Our goal is to make our opponent passive”. Therefore, this begs the question, "What are investors missing when they commit to passive investing as a way to protect and grow their capital?"

To begin with, there are thousands of indexes and even more index funds that track them. How do you choose the best one for your situation? If you do all your own research to select an index fund, you have, in essence, become an active manager. Few individual investors have the time, or more importantly, the expertise for this.

Markets, by nature, move up and down. Sometimes down comes over 2-3-5 years, and sometimes it comes in a single, staggering chop. Who steps in to mitigate the damage, and who takes action to re-engage once things have settled down? That would be the individual investor once again.

Finally, there is the issue of the tax ramifications of passive investing. Index funds and passive asset allocation create transactions regularly through constant rebalancing. This causes batches of buying and selling, which causes capital gains to be realized and distributed to the index fund shareholder at the end of the year, regardless of the consequences.

Investors need to spend more time understanding their investment strategy, asset allocation, and investment selection to be prepared for the multiple risks that come along with it. This will improve the odds of reaching their long-term goals as well as provide a basis for course corrections, as well as stick-to-it-ness when the time arrives.

*Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. Asset allocation, which is driven by complex mathematical models, should not be confused with the much simpler concept of diversification. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns and it is an investment strategy that will not guarantee a profit or protect you from loss.

If you lack the time and expertise to actively allocate your investments and are sensitive to the potential pitfalls of passive investing, a good place to start is to speak with an experienced financial advisor who can act as an active asset allocator.

Download your copy of A Case for Active Risk Management, to learn how active management can mean the difference between pursuing your financial goals and lifestyle dreams by embracing the precision of a well-defined, active strategy.

Download Your Complimentary Brochure Here

--

About the Author

Jack Brkich III, is the president and founder of JMB Financial Managers. A Certified Financial Planner, Jack is a trusted advisor and resource for business owners, individuals, and families. His advice about wealth creation and preservation techniques have appeared in publications including The Los Angeles Times, NASDAQ, Investopedia, and The Wall Street Journal. To learn more visit https://www.jmbfinmgrs.com/.

Jack Brkich III, is the president and founder of JMB Financial Managers. A Certified Financial Planner, Jack is a trusted advisor and resource for business owners, individuals, and families. His advice about wealth creation and preservation techniques have appeared in publications including The Los Angeles Times, NASDAQ, Investopedia, and The Wall Street Journal. To learn more visit https://www.jmbfinmgrs.com/.

Connect with Jack on LinkedIn or follow him on Twitter.

Disclosure: The views are those of Jack Brkich III, CFP and should not be construed as investment advice. All economic and performance information is historical and past performance is not indicative of future results. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and, when sold or redeemed, you may receive more or less than originally invested. No system or financial planning strategy can guarantee future results. Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing. Asset allocation, which is driven by complex mathematical models, should not be confused with the much simpler concept of diversification. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns and it is an investment strategy that will not guarantee a profit or protect you from loss. Exchange-traded funds are sold only by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. Exchange-traded funds incur trading and commission costs similar to stocks and frequent trading can negate the lower cost structure of an ETF. The prospectus contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

JMB Financial Managers Mid-Year Review for 2025

Click the button below to download a pdf of insights and predictions for the rest of the year.